Why physical risk scores alone are insufficient for strategic investment decision-making — and what a more complete picture looks like.

Physical Risk is Not Enough

Climate risk analytics have made significant progress over the past decade. Today, institutional investors and asset managers can access hazard scores for flood, heat, drought, fire, and wind — mapped to assets anywhere on Earth across multiple emissions scenarios and time horizons. This is a genuine advance.

But there is a critical gap in most of these assessments: they measure the intensity of a hazard without accounting for what a location has done — or is doing — to manage it.

Consider two coastal assets, each sitting in an area with an identical 1,000-year coastal flood inundation level of 35cm. On a standard physical risk map, they look equivalent. But one is protected by a robust seawall and a functioning municipal drainage network. The other has no flood barrier and limited infrastructure. The actual expected damage to those two assets is not the same. Not even close.

Physical hazard risk is a necessary input. It is not a sufficient output.

For ESG and sustainability teams at real asset managers, this gap creates a compounding problem. Overestimating risk at resilient locations leads to mispriced assets and missed investment opportunities. Underestimating risk at vulnerable ones creates unhedged exposure. Either way, capital allocation suffers.

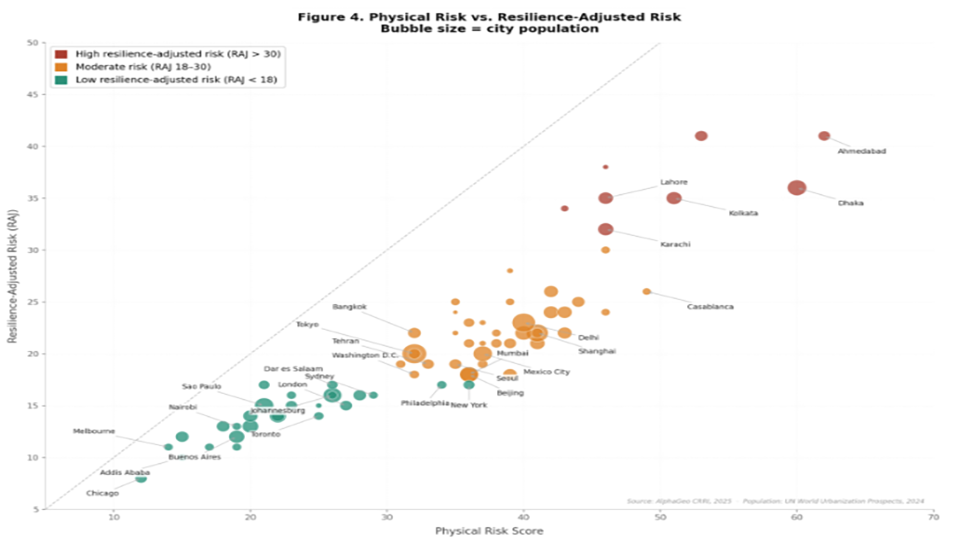

What is Resilience-adjusted Risk?

Resilience-adjusted risk is a methodology that incorporates the effect of local adaptation measures directly into the risk calculation — rather than treating them as a qualitative footnote.

AlphaGeo’s Climate Risk & Resilience Index (CRRI) applies this framework across six climate hazard categories: heat stress, drought, inland flooding, coastal flooding, hurricane wind, and wildfire. For each hazard, we first calculate the physical risk baseline using established climate models and emissions scenarios (SSP245, SSP370, SSP585). Then, we apply a location-specific adaptation offset that reflects both the built environment and the broader societal infrastructure at that location.

The result is two distinct scores for every asset:

- Physical Climate Risk Score: The theoretical hazard baseline, derived from global climate models. This is the “what could happen” number.

- Resilience-Adjusted Risk Score: The likely actual risk after accounting for the adaptation capacity of the location. This is the “what is likely to happen” number.

The gap between these two scores is where investment insight lives.

How the Offset is Calculated

The adaptation offset is not an estimate or a qualitative judgment. It is computed from hyper-local geospatial data across more than 20 hazard-specific adaptation measures — sourced from peer-reviewed datasets, well-documented repositories, and well-established global data providers.

For each hazard, AlphaGeo’s Global Adaptation Layer maps the specific infrastructure and environmental conditions that reduce damage intensity at that location. Examples include:

- Inland flooding: Proximity to drainage systems, surface porosity, and flood management infrastructure.

- Coastal flooding: Presence and coverage of coastal barriers, proximity to natural buffers such as wetlands and mangroves.

- Heat stress: Building density, urban greenery coverage, and the urban heat island effect.

- Wildfire: Proximity to fire response stations, fire prevention infrastructure, and burnable fuel load.

- Drought: Access to water treatment and storage infrastructure, and water supply resilience.

- Hurricane wind: Building strength and construction standards, and proximity to flood management systems.

After applying hazard-specific adaptation offsets, an additional adjustment accounts for societal resilience — including local income levels, health infrastructure, education, and government effectiveness. Locations with stronger societal foundations have greater capacity to respond to and recover from climate shocks, which meaningfully reduces expected damage even when physical adaptation infrastructure is comparable.

The Global Adaptation Layer is engineered at up to 30 meters in spatial resolution — enabling asset-level, not just city-level, insight into adaptation capacity.

Why this Matters for Capital Allocation

The practical effect of resilience adjustment can be substantial. In AlphaGeo’s framework, a location with a physical coastal flood risk score of 40/100 may carry a resilience-adjusted score as low as 14/100 when robust coastal defenses and strong societal infrastructure are in place. That shift — from medium risk to low risk — carries real financial implications: lower expected damage ratios, reduced insurance cost trajectories, lower CapEx requirements for climate retrofits, and more defensible asset valuations.

Conversely, a location with a moderate physical risk score but weak adaptation infrastructure may carry a resilience-adjusted score that is nearly equivalent to its physical baseline — or worse when societal resilience is fragile. These are the locations where conventional risk assessments give investors false comfort.

For ESG and sustainability teams, the implications extend beyond individual asset analysis:

- Portfolio construction: Resilience-adjusted scores allow for more accurate comparison of assets across geographies. A flood-prone asset in the Netherlands may carry lower effective risk than a similar asset in a less-adapted market.

- Regulatory reporting: Frameworks such as TCFD, IFRS S2, and the EU Taxonomy increasingly require disclosure of physical risk. Resilience-adjusted metrics provide a more defensible and accurate basis for those disclosures than raw hazard scores.

- Site selection and acquisition: Resilience data enables screening not just for current risk but for adaptation trajectory — identifying locations where resilience infrastructure is improving, and where it is not.

- Valuation integrity: Risk assessments feed directly into discount rates, insurance cost assumptions, and CapEx budgets. More accurate risk inputs produce more accurate valuations.

From Assessment to Action

A resilience-adjusted risk score is not just a more accurate number. It is a more actionable one.

Because the score is built from specific adaptation features — rather than a black-box aggregate — it tells you precisely which factors are driving the offset between physical and effective risk. For a given asset, you can see that flood risk is being reduced by proximity to drainage systems but that a low score on direct flood barrier coverage is limiting the total offset. That is not an abstract data point. It is a CapEx thesis.

AlphaGeo’s Climate Financial Impact Metrics (CFIM) translate this directly into financial terms: projected changes in insurance premiums, utility costs, and retrofit CapEx requirements — expressed as annual rates of change and percentages of net income. These metrics are designed to integrate into standard financial models, including Discounted Cash Flow analysis, enabling climate-adjusted valuation rather than climate-qualified narrative.

The question is not just “how risky is this asset?” but “what would it cost to make it less risky — and is that investment priced in?”

The Ground Truth Imperative

Climate risk analytics are only as useful as they are accurate. A score that measures hazard intensity without adaptation context is, at best, a starting point. For investors making long-horizon allocation decisions — where terminal value, insurance markets, and regulatory environments will all be shaped by climate outcomes — a starting point is not enough.

Resilience-adjusted risk is not a softer view of climate exposure. In many cases, it surfaces risk that conventional models miss entirely: assets in jurisdictions where adaptation infrastructure is deteriorating, where societal resilience is eroding, or where current adaptation measures are insufficient to offset projected changes in hazard intensity.

The goal is not to minimize climate risk on paper. It is to understand it accurately — so that capital can be allocated with confidence, assets can be managed with precision, and resilience can be treated as the investable quality it is.